|

|||||||||||||||||||||

|

| ||||||||||||||||||||

| |||||||||||||||||||||

|

|

|

|

||||||||||||||||||

|

|||||||||||||||||||||

|

|||||||||||||||||||||

| Banks do not Operate in a Competive Market - Summary of Problems and Solutions | |||||||||||||||||||||

|

Summary Introduction

The resulting paradox of the recent banking collapse is that ineviatable changes to the system will ultimately

cause the banks to be less wealthy in the future. The developement of society will naturally create the forces that change it for

the better. Occasionally at the detriment to those that caused any issues and problems in the first place that initiated the changes

in society required to make it better. If these changes do not happen, then the banks will be free to exhaust the economy again, because

the key questions have not been asked or answered about their methods or the system. It is time to understand the reasons why we are

where we are and make the decision to update the financial system to benefit the nation.

What Is Needed

Fractional banking is necessary in the economic system, because without it, there would be no mortgages. Fractional banking push house prices forever upward, where there is no upper limit to new cash mortgages. We need these systems and money producing methods to service money supply, but we must control it to service the wider aspects of the economy. |

|||||||||||||||||||||

|

|||||||||||||||||||||

|

Market Balance

Market place buying and selling has a hierarchical nature, the first is the primary market controller and leader, and

the other is the second. The autocracy of primary market ownership will always have power over the market secondary participants.

Introducing rules that will control the primary market owner of mortgage supply will cause price fixing problems and diminish motiviation

within the business. Except that the demand for housing will drive the system supplying new money for new mortgages.

Credit

Review

Denial of a loan or mortgage can be examined by conducting a credit review. This is held after loans are declined which is after

the event and too late for business to take place. New legislation is needed to make it a transparent and compulsory decision before,

during and after the credit process to buy houses. Too accompany this, banks calling in default loans must follow judicicial proceedings.

Improved Interests

The system can be bettered so that less of an amount of interest money is taken from the economy and from

people who are forced to endure the efforts required to afford the payments, whilst those that make these interest payments gain no

benefit and or advantage from the present system. A new better system will advance an economy quicker and safer because it will be

built upon firmer foundations, rather than taking money out of future economic activity that has yet to happen just to pay for bank

profits.

|

|||||||||||||||||||||

|

|||||||||||||||||||||

|

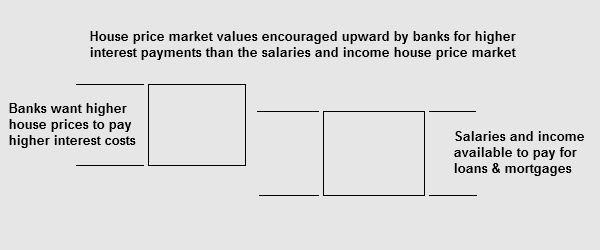

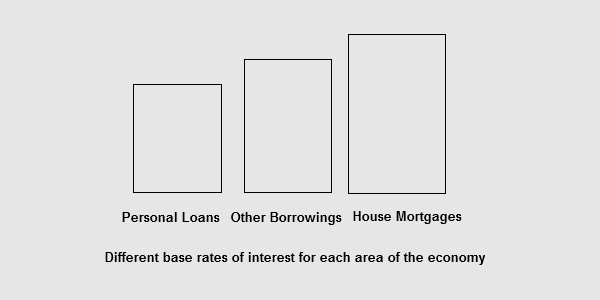

Interests Adjustments

The central bank of the nation country adjusts the standard base interest rate to control the economy, this affects

more than the housing market, it also has an effect upon the domestic economy. This control is too far removed and remote to be applied

and implemented successfully toward the aim of correcting over heating parts of the economy. The economy must be separated into its

constituent parts and treated accordingly.

Hierarchial Market

Administration of credit should be standardised across the industry

with differently adjusted interest base rates set according to each area of the economy, this will inhibit the market pressures that

banks use to inflate profits at the detiment of the customer base. These credit controlling profit driven markets have too steep a

hierarchial lean to benefit the economy, while the hierarchial market controller is at the power base of economic policy direction.

Civilisation does not want the problems associated with this hierarchial lean, so it is time for a new rebuild.

|

|||||||||||||||||||||

|

|||||||||||||||||||||

|

Information Necessary

Central banks are not dissimilar from the Federal Reserve Bank in the US, which is a private for profit company

that receives interest payments made to them from the general wealth and work of the nation and then transfers them into profits for

the benefit of the shareholders of the Federal Reserve private company. This system was brought into law by those that benefit from

it and is now ready for change. Do nothing and government debt will remain a continual phenomemum and taxes will be paid to creditors

interest charges.

Central Banks are Private Businesses for Profit Most central banks are similar. In the US, the Federal Reserve is neither federal nor reserve, this private for profit bank prints bonds and cash to lend to the government with interest payments due. The US treasury should be in charge of and control cash supply, but it is not. This situation has been addressed previously with the introduction of the Greenback Dollar in the mid 1800s in the US, and reportedly caused the assasination of Abraham Lincoln. It was launched and introduced to elliminate this central bank problem but was not successfully implemented because Lincoln was killed. The old feudal system remained in place. Central Banks or Government Treasury The Federal Reserve Act of 1913 granted it the legal authority to issue Federal Reserve Notes known as the U.S. Dollar. The Phelan Act of 1920 gave unfettered permission to major banks to control the smaller banks for their own profit making interests. The larger banks then called in loans from the smaller banks, which could not pay immediately, and so the Great Depression was initiated. This was done in such a way that several years later, the larger banks were able to buy up large swathes of default payment lands and property at knock down prices, that they were then able to sell later at a profit, and or rent out to the farmers it once was belonged to. The survival of the fittest in the sphere of banking became normalised. |

|||||||||||||||||||||

|

Summary Solution

Government bonds will be given multiple values within an international framework. The more money that is successfully paid in interest due upon bonds, then the more is returned in deserved credit worthiness. Consistent repayments to be reclassified on an on going basis to help towards a loyalty points system where short term debt transfers to long tem debt and therefore attract lower annual interest payments. It is now the responsibility of the creditors to decide if the debt of a country will soon become long term debt and not payable short term. Interest payments to continue at lower levels for a longer period of time. Solution Summary A loyalty card system supercedes a market value system because market shifts are inhibited to reflect cash values only. Economic acitvity and political set up and debt ratio are all counted within credit ratings and associated interest rates with government bond values. By rolling over short term bonds into long term bonds, they keep their value as they will return the same quantity of value for money over time. These activities are presently in a market value system, where a credit rating is given and used by investment companies to value the credit worthiness of a country, these system values can be improved by adding more features to the credit rating with a loyalty points system. Solutions New money debts and newly commissioned funds that are now debts to high street banks can now be reconsidered shelved with no interest accrueing and to be paid much later to in order to allow the relaunch of the economy in the meantime. Housing costs and personal income must be associated together within a market adjusted system and not controlled to promote bank profits. Supplement

material is available to publish on request. More to follow. Thank you.

improvedworld@gmail.com

twitter facebook cliffjohn

|

|||||||||||||||||||||